With our mid-year update, the banking industry consolidation continues:

5,303 banking charters remain with over 97% being Community Banks (Total Assets < $10 billion);

Net reduction of 239, or 4.3% over the latest four quarters;

Bank mergers continue with just under 250 over latest four quarters;

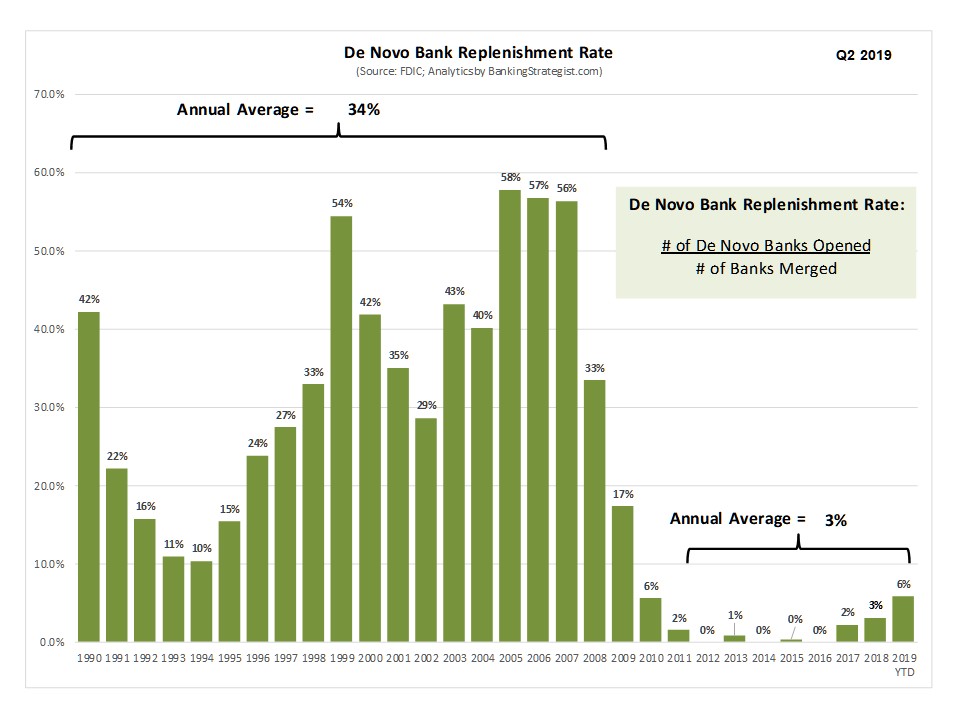

De Novo Bank Replenishment Rate only 3% (i.e., de novo banks replacing only 3 percent of banks lost to mergers); and

Impact of decline in bank charters primarily felt by Community Banks and in smaller markets.

Of the 248 bank charter decline over the last four quarters, only 9 charters were replenished by de novo bank start-ups. There was only one bank failure during this timeframe. The net attrition rate of 4.3% is comparable to historical averages.

Bank mergers are a key component of many banker’s strategic planning currently and have been over the last several decades. And bank merger activity continues today with approximately 247 completed over the last four quarters. While down significantly from the average of 482 mergers from 1990 to 2008, merger activity is comparable to that occurring over the last several years.

De novo banking is no longer a significant activity to rebuild the ranks of community banks. If you look at the De Novo Bank Replenishment Rate, this phenomenon is clear. We will define this metric as the number of de novo banks opened divided by the number of banks that have merged. From 1990 through 2008, the De Novo Bank Replenishment Rate averaged 34% - that is, for every 100 bank mergers, there were 34 de novo start-ups that opened. Over the last several years, this metric averaged only 3%.

The decline in the number of banking charters is predominantly occurring among smaller Community Banks - banks with Total Assets of less than $250 million. The number of banks in these asset classes dropped by 238. There was net growth in Community Banks with Total Assets between $1 billion and $10 billion.

And where geographically is this consolidation occurring? Illinois and Texas had significant reductions of 22 and 19, respectively. Six states had declines in the number of banks by 10 or more: Iowa, Minnesota, Wisconsin, Kansas, California and Pennsylvania.

And does the size of the market have relevance? While the smallest counties had sizable declines, larger population areas also had fewer banks. If we use County population as the measure, there was a drop of 51 banks headquartered in markets with populations greater than 750,000. And, at the other end of the spectrum, there was a reduction of 99 banks headquartered in counties with populations of less than 50,000. This continued decline in smaller, rural markets is concerning, given the importance of local, community banks to these markets.

The banking industry consolidation continues its decades long run with no end in sight. Bank mergers are ongoing. Bank Failures will occur from time to time. The historic replenishment role that de novo banks played is all, but gone. Look for our semi-annual updates. And for more data and analytics on the banking industry, go to www.BankingStrategist.com.